This recession call is coming from inside the house.

The Bank of Canada has highlighted elevated household debt and imbalances within the nation’s real estate market as the two chief vulnerabilities to the financial system in the event of a recession.

But what could trigger such a downturn? Macquarie Capital Markets offers one simple answer: the housing market itself -- highlighting that the share of employment tied to construction as well as finance, insurance and real estate is nearly two standard deviations above its long-term average.

#lazy-img-328065795:before{padding-top:56.25%;}Tighter mortgage rules and higher interest rates have weighed on activity in formerly high-flying Canadian housing markets, with home sales in Toronto having their worst start to the year since 2009.

Top Insurance Stocks To Buy For 2018: Aon Corporation(AON)

Advisors' Opinion:- [By Stephan Byrd]

US Bancorp DE raised its stake in shares of Aon (NYSE:AON) by 3.0% in the first quarter, according to the company in its most recent disclosure with the SEC. The firm owned 40,448 shares of the financial services provider’s stock after acquiring an additional 1,178 shares during the quarter. US Bancorp DE’s holdings in AON were worth $5,676,000 as of its most recent filing with the SEC.

- [By Joseph Griffin]

AON (NYSE:AON) had its price target hoisted by Citigroup from $160.00 to $165.00 in a report issued on Tuesday morning. They currently have a buy rating on the financial services provider’s stock.

- [By Max Byerly]

State of Wisconsin Investment Board decreased its holdings in shares of Aon (NYSE:AON) by 9.2% in the 1st quarter, Holdings Channel reports. The fund owned 384,127 shares of the financial services provider’s stock after selling 38,942 shares during the quarter. State of Wisconsin Investment Board’s holdings in AON were worth $53,905,000 at the end of the most recent quarter.

- [By Lisa Levin] Companies Reporting Before The Bell Celgene Corporation (NASDAQ: CELG) is projected to report quarterly earnings at $1.96 per share on revenue of $3.46 billion. Aon plc (NYSE: AON) is expected to report quarterly earnings at $2.8 per share on revenue of $2.93 billion. American Axle & Manufacturing Holdings, Inc. (NYSE: AXL) is estimated to report quarterly earnings at $0.81 per share on revenue of $1.75 billion. Alibaba Group Holding Limited (NYSE: BABA) is expected to report quarterly earnings at $0.88 per share on revenue of $9.27 billion. LifePoint Health, Inc. (NASDAQ: LPNT) is projected to report quarterly earnings at $1.13 per share on revenue of $1.62 billion. V.F. Corporation (NYSE: VFC) is estimated to report quarterly earnings at $0.65 per share on revenue of $2.90 billion. Newell Brands Inc. (NYSE: NWL) is expected to report quarterly earnings at $0.26 per share on revenue of $3.05 billion. Titan International, Inc. (NYSE: TWI) is projected to report quarterly earnings at $0.04 per share on revenue of $407.27 million. Boise Cascade Company (NYSE: BCC) is expected to report quarterly earnings at $0.45 per share on revenue of $1.09 billion. Cheniere Energy, Inc. (NYSE: LNG) is estimated to report quarterly earnings at $0.39 per share on revenue of $1.59 billion. Cboe Global Markets, Inc. (NASDAQ: CBOE) is projected to report quarterly earnings at $1.24 per share on revenue of $308.05 million. ITT Inc. (NYSE: ITT) is estimated to report quarterly earnings at $0.73 per share on revenue of $683.96 million. Fred's, Inc. (NASDAQ: FRED) is expected to report quarterly loss at $0.19 per share on revenue of $551.00 million. Virtu Financial, Inc. (NASDAQ: VIRT) is projected to report quarterly earnings at $0.52 per share on revenue of $288.31 million. Cheniere Energy Partners, L.P. (NYSE: CQP) is expected to report quarterly earnings at $0.57 per share on revenue of $1.38 billion. Genesis Energy, L.P

Top Insurance Stocks To Buy For 2018: Prudential Financial Inc.(PRU)

Advisors' Opinion:- [By Max Byerly]

Flippin Bruce & Porter Inc. grew its holdings in shares of Prudential Financial (NYSE:PRU) by 2.3% in the 1st quarter, according to its most recent disclosure with the Securities and Exchange Commission (SEC). The institutional investor owned 61,363 shares of the financial services provider’s stock after acquiring an additional 1,391 shares during the period. Flippin Bruce & Porter Inc.’s holdings in Prudential Financial were worth $6,354,000 as of its most recent SEC filing.

- [By Zacks]

Well, given the growing demand for securitized mortgage deals, Barclays plans to package and sell these Irish loans over the next two months. The group of investors that has shown interest in buying residential mortgage backed securities includes M&G Investments, the investment management division of British insurer Prudential Plc (NYSE: PRU) and Pacific Investment Management Co. ("PIMCO").

- [By Jason Hall, Chuck Saletta, and Reuben Gregg Brewer]

But that doesn't mean you need to make risky bets to capture solid returns, either, and buying solid companies at reasonable prices can help create a margin of safety and improve your returns, while also decreasing your risk of permanent losses. Three stocks that meet these criteria are small healthcare real-estate specialist�Caretrust REIT Inc�(NASDAQ:CTRE), financial services giant�Prudential Financial Inc�(NYSE:PRU), and energy behemoth�ExxonMobil Corporation�(NYSE:XOM).�

- [By Joseph Griffin]

These are some of the headlines that may have effected Accern Sentiment Analysis’s analysis:

Get Prudential Financial alerts: Prudential (PUK) Presents At 2018 Deutsche Bank Annual Global Financial Services Conference – Slideshow (seekingalpha.com) Leston Welsh joins Prudential Group Insurance as head of Disability and Absence Management (finance.yahoo.com) Contrasting Prudential Financial (PRU) & Old Mutual (ODMTY) (americanbankingnews.com) Prudential again accused with unauthorised money deduction (vir.com.vn) An Application for the Trademark ��MULLINTBG�� Has Been Filed by Prudential Insurance Company (insurancenewsnet.com)Prudential Financial traded down $5.05, hitting $94.97, during midday trading on Tuesday, MarketBeat Ratings reports. 2,919,216 shares of the company’s stock were exchanged, compared to its average volume of 2,144,103. The company has a current ratio of 0.12, a quick ratio of 0.12 and a debt-to-equity ratio of 0.35. The firm has a market cap of $42.01 billion, a PE ratio of 8.98, a P/E/G ratio of 0.97 and a beta of 1.52. Prudential Financial has a one year low of $94.51 and a one year high of $127.14.

- [By Chuck Saletta]

Prudential Financial (NYSE:PRU) takes such pride in its rock-solid financial condition that it uses an actual rock -- the Rock of Gibraltar�-- as its corporate symbol. Prudential Financial backs up that claim with a balance sheet that has more cash, cash equivalents, and short-term investments�than total debt on it. It also claims a debt-to-equity ratio around 0.6 and a current ratio around 1.0�, which are further signs of a solid financial condition.

Top Insurance Stocks To Buy For 2018: American International Group Inc.(AIG)

Advisors' Opinion:- [By Max Byerly]

These are some of the media stories that may have effected Accern’s rankings:

Get American International Group alerts: AIG’s loss for European business worsens in 2017 (businessinsurance.com) $1.26 EPS Expected for American International Group (AIG) This Quarter (americanbankingnews.com) UBS: Buy AIG After Earnings Estimates ‘Bottom Out’ (finance.yahoo.com) American International Group (AIG) Stock Rating Upgraded by UBS (americanbankingnews.com) American International Group (AIG) Receives Average Recommendation of “Hold” from Analysts (americanbankingnews.com)American International Group traded up $0.36, hitting $55.15, during mid-day trading on Friday, MarketBeat.com reports. The stock had a trading volume of 9,821,608 shares, compared to its average volume of 6,828,715. The company has a debt-to-equity ratio of 0.53, a current ratio of 0.27 and a quick ratio of 0.27. American International Group has a 1-year low of $49.57 and a 1-year high of $67.30. The firm has a market cap of $49.51 billion, a P/E ratio of 22.98, a PEG ratio of 1.01 and a beta of 1.24.

- [By ]

Insurance company American International Group Inc. (AIG) stock fell 5.3% as harsh winter weather weighed on profits. But the company's long-term care exposure is relatively minimal.

- [By Logan Wallace]

Sentry Investment Management LLC lessened its holdings in American International Group (NYSE:AIG) by 8.6% during the first quarter, HoldingsChannel reports. The firm owned 64,968 shares of the insurance provider’s stock after selling 6,147 shares during the quarter. Sentry Investment Management LLC’s holdings in American International Group were worth $3,536,000 at the end of the most recent reporting period.

Top Insurance Stocks To Buy For 2018: Principal Financial Group Inc(PFG)

Advisors' Opinion:- [By WWW.GURUFOCUS.COM]

For the details of Stilwell Value LLC's stock buys and sells, go to http://www.gurufocus.com/StockBuy.php?GuruName=Stilwell+Value+LLC

These are the top 5 holdings of Stilwell Value LLCOFG Bancorp (OFG) - 1,614,868 shares, 14.1% of the total portfolio. Kingsway Financial Services Inc (KFS) - 3,780,889 shares, 12.63% of the total portfolio. HopFed Bancorp Inc (HFBC) - 627,128 shares, 7.62% of the total portfolio. Alcentra Capital Corp (ABDC) - 1,251,324 shares, 7.27% of the total portfolio. Shares added by 20.66%Sound Financial Bancorp Inc (SFBC) - 228,600 shares, 7.02% of th - [By Joseph Griffin]

KBC Group NV lowered its position in shares of Principal Financial Group Inc (NYSE:PFG) by 41.4% in the 1st quarter, according to its most recent disclosure with the SEC. The fund owned 201,808 shares of the financial services provider’s stock after selling 142,313 shares during the period. KBC Group NV’s holdings in Principal Financial Group were worth $12,292,000 as of its most recent filing with the SEC.

- [By Max Byerly]

Shore Capital reissued their hold rating on shares of Provident Financial (LON:PFG) in a report issued on Thursday.

PFG has been the subject of several other reports. Liberum Capital reissued a sell rating and set a GBX 483 ($6.48) price objective on shares of Provident Financial in a research note on Monday, February 26th. Peel Hunt reissued a hold rating and set a GBX 870 ($11.67) price objective on shares of Provident Financial in a research note on Tuesday, February 27th. JPMorgan Chase & Co. reduced their price objective on Provident Financial from GBX 1,100 ($14.76) to GBX 750 ($10.06) and set a neutral rating for the company in a research note on Thursday, May 10th. Barclays reissued an underweight rating and set a GBX 584 ($7.84) price objective on shares of Provident Financial in a research note on Wednesday, January 31st. Finally, Societe Generale lowered Provident Financial to a hold rating and set a GBX 1,050 ($14.09) price objective for the company. in a research note on Wednesday, February 28th. Two investment analysts have rated the stock with a sell rating, eleven have assigned a hold rating and two have assigned a buy rating to the company’s stock. Provident Financial presently has a consensus rating of Hold and a consensus price target of GBX 1,190.14 ($15.97).

- [By Shane Hupp]

These are some of the news articles that may have impacted Accern’s scoring:

Get Principal Financial Group alerts: Principal Financial Group (PFG) Approves New $300M Buyback (streetinsider.com) Principal Financial Group (PFG) Announces Share Repurchase Plan (americanbankingnews.com) Is Principal Large Cap Growth I Institutional (PLGIX) a Strong Mutual Fund Pick Right Now? (finance.yahoo.com) Principal Financial Group is Oversold (nasdaq.com) Principal Names New Chief Human Resources Officer (finance.yahoo.com)Several equities analysts have recently commented on PFG shares. Morgan Stanley decreased their target price on Principal Financial Group from $79.00 to $77.00 and set an “equal weight” rating on the stock in a research report on Thursday, April 5th. Wells Fargo reaffirmed a “market perform” rating and issued a $76.00 target price on shares of Principal Financial Group in a research report on Monday, January 8th. Credit Suisse Group started coverage on Principal Financial Group in a research report on Wednesday, April 25th. They issued a “neutral” rating and a $62.00 target price on the stock. Bank of America started coverage on Principal Financial Group in a research report on Monday, March 26th. They issued a “neutral” rating and a $65.00 target price on the stock. Finally, UBS started coverage on Principal Financial Group in a research report on Friday, March 2nd. They issued a “neutral” rating and a $69.00 target price on the stock. Two research analysts have rated the stock with a sell rating, seven have given a hold rating and three have issued a buy rating to the company. Principal Financial Group currently has an average rating of “Hold” and an average price target of $71.18.

Expected iPhone X and X Plus. Source: Mac Rumors

Expected iPhone X and X Plus. Source: Mac Rumors Since the earnings call on May 1, Apple is up over 12% and is very close to its all-time high. Analyst coverage has turned a little more bullish, with an average price target of $195. Despite the price target, it's only natural to wonder how much upside is left.

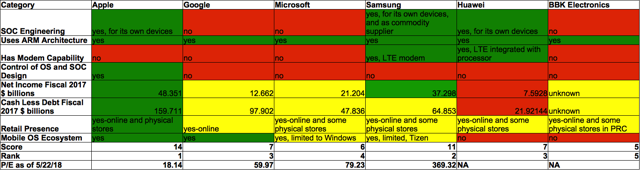

Since the earnings call on May 1, Apple is up over 12% and is very close to its all-time high. Analyst coverage has turned a little more bullish, with an average price target of $195. Despite the price target, it's only natural to wonder how much upside is left. In the peer group, I include companies that provide competing operating systems, such as Google (GOOG) (NASDAQ:GOOGL) and Microsoft (MSFT), as well as the most important device manufacturers, Samsung, Huawei, and BK Electronics, home of the OPPO and vivo brands.

In the peer group, I include companies that provide competing operating systems, such as Google (GOOG) (NASDAQ:GOOGL) and Microsoft (MSFT), as well as the most important device manufacturers, Samsung, Huawei, and BK Electronics, home of the OPPO and vivo brands. Apple's custom SOCs have been instrumental in the creation of new products such as Apple Watch and Air Pods. There's additional synergy due to the fact that Apple's operating systems developers have access to intimate knowledge about the processors that they wouldn't have if the processors were developed by a separate company. This allows its operating systems to be better optimized and integrated with its hardware.

Apple's custom SOCs have been instrumental in the creation of new products such as Apple Watch and Air Pods. There's additional synergy due to the fact that Apple's operating systems developers have access to intimate knowledge about the processors that they wouldn't have if the processors were developed by a separate company. This allows its operating systems to be better optimized and integrated with its hardware. DCF fair value

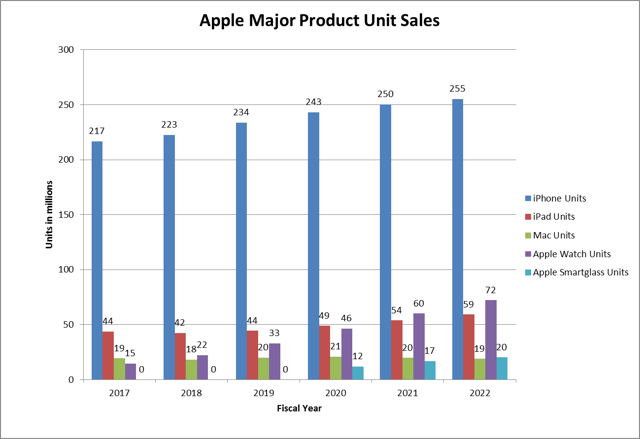

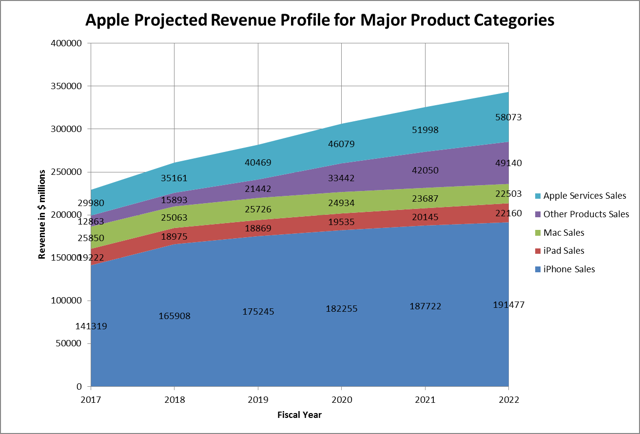

DCF fair value  The finbox model yields a share fair value of $193.03. In modifying the profiles, I perform a ��ground up�� estimate of revenue contributors, based on the product unit growth shown earlier, as well as other inputs.

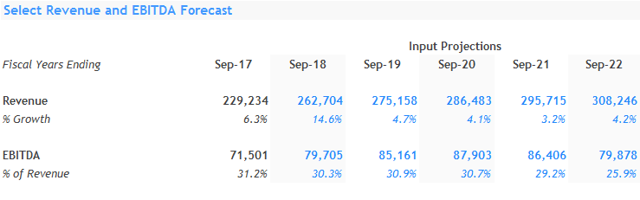

The finbox model yields a share fair value of $193.03. In modifying the profiles, I perform a ��ground up�� estimate of revenue contributors, based on the product unit growth shown earlier, as well as other inputs. This yields modified revenue and EBITDA profiles shown below:

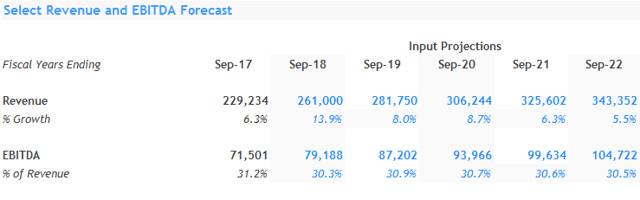

This yields modified revenue and EBITDA profiles shown below: The EBITDA profile reflects my expectation that Apple's margins will not decline very much over the five-year period. The resultant share fair value is $239.89. This gives an upside of about 29% compared to the current share price of about $186.

The EBITDA profile reflects my expectation that Apple's margins will not decline very much over the five-year period. The resultant share fair value is $239.89. This gives an upside of about 29% compared to the current share price of about $186.