Rethink Technology business briefs for May 23, 2018.

Earnings assuages fears, encourages upgrades

Expected iPhone X and X Plus. Source: Mac Rumors

Expected iPhone X and X Plus. Source: Mac Rumors

I wrote Apple: No Need To Panic on April 27, a few days before Apple's (AAPL) fiscal 2018 Q2 earnings release. At the time, fears of a meltdown in iPhone X sales were at a fever pitch. I could not say absolutely that the fears were unjustified, but I did critique a couple of the more negative articles that also bore on two other members of the Rethink Technology Portfolio, ASML Holding (ASML) and Taiwan Semiconductor Manufacturing Company (TSM). In retrospect, it was one of the most prescient articles I've ever written.

The fears of tanking iPhone X sales proved groundless, as Apple's CEO Tim Cook emphasized that iPhone X has outsold every other iPhone model since its introduction, something that had never happened before.

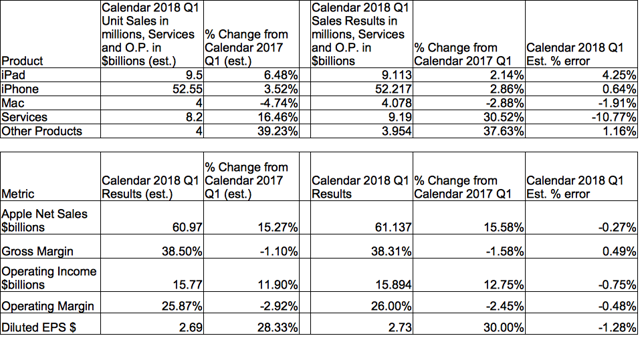

My earnings estimates, published for subscribers, came about as close as I've ever done:

Since the earnings call on May 1, Apple is up over 12% and is very close to its all-time high. Analyst coverage has turned a little more bullish, with an average price target of $195. Despite the price target, it's only natural to wonder how much upside is left.

Since the earnings call on May 1, Apple is up over 12% and is very close to its all-time high. Analyst coverage has turned a little more bullish, with an average price target of $195. Despite the price target, it's only natural to wonder how much upside is left.

I came away from the earnings report convinced that the answer is ��a lot,�� but I needed to revise my investment case for Apple. For each member of the RT Portfolio, I create an Investment Case Report, setting forth my analysis and expectations for a given company. The RT Portfolio reflects my personal portfolio, so I always have skin in the game. I feel this forces me to pay careful attention to the Portfolio companies and continually reevaluate them as long-term investments.

I first wrote the Investment Case for Apple over a year ago, and although I update the report monthly for subscribers, I realized that it needed to be substantially rewritten. What follows are highlights from that much revised report.

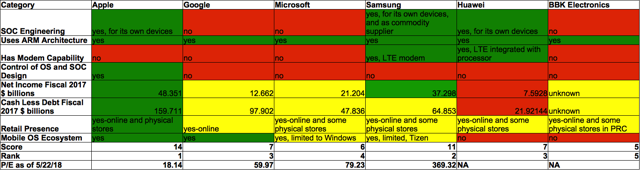

Apple's still low valuation, relative to peersOne of the things I do as part of compiling the investment case for a company is a competitive assessment. I generally look for companies that are leaders in their key market or markets. Apple's key market is mobile devices, so my competitive assessment for Apple emphasizes important technologies in the mobile device, such as the processor and the operating system.

I also consider other factors related to profitability and financial strength. My competitive assessment for Apple is shown in the table below.

In the peer group, I include companies that provide competing operating systems, such as Google (GOOG) (NASDAQ:GOOGL) and Microsoft (MSFT), as well as the most important device manufacturers, Samsung, Huawei, and BK Electronics, home of the OPPO and vivo brands.

In the peer group, I include companies that provide competing operating systems, such as Google (GOOG) (NASDAQ:GOOGL) and Microsoft (MSFT), as well as the most important device manufacturers, Samsung, Huawei, and BK Electronics, home of the OPPO and vivo brands.

The color coding reflects an admittedly subjective assessment of the situation of each company relative to a given criterion. Green receives 2 points, yellow, 1 point, and red, 0 points. Incidentally, following Microsoft's abandonment of Windows Phone, I had to drop its rating in the Mobile OS Ecosystem to yellow.

I've also included the TTM P/E ratios for the four publicly traded companies. Apple, of course, stands out for its very low valuation.

Growth driversApple's low valuation doesn't automatically mean that it's a bargain. Apple's valuation reflects the low expectations of the market, as well as many analysts. For many years, there was a school of thought that regarded iPhone as merely a fad. The argument went that iPhone sales would collapse once it ceased to be fashionable.

That argument has kind of fallen by the wayside in favor of more directly applicable observations such as ��smartphone sales have stagnated�� and ��Apple is too dependent on iPhone.�� Both arguments are true, in the near term, but ignore factors that might make them untrue in the long term.

In iPhone X, Apple has captured many of the technologies that will drive iPhone sales growth in the next few years. These are Apple's superior mobile processors, OLED displays, and 3D sensing, both for user facing and world facing applications. The popularity of iPhone X suggests that unit volumes will increase y/y once Apple makes the features of X more affordable, which it is expected to do this September.

Another growth driver for Apple, and the entire mobile device industry, is expected to be 5G. 5G is a complex technology that will use multiple radio bands, including some in the millimeter wave region. 5G will provide greater data speeds (above 1 Gbit/sec, download) as well as greatly enhanced network capacity, which is currently the key practical limiter to real world performance.

5G also will be an enabler of the Internet of Things (IoT) and wearables of various types. The 5G standard provides for new types of low power data connections that reduce the power drain on mobile devices.

5G adoption by carriers is moving much faster than expected, even a year ago. This probably reflects the need to expand capacity (especially in the face of an expected increase in IoT devices) more than it does the desire to provide users with higher speed connections. Both AT&T and Verizon have announced plans for initial deployments this year in the U.S.

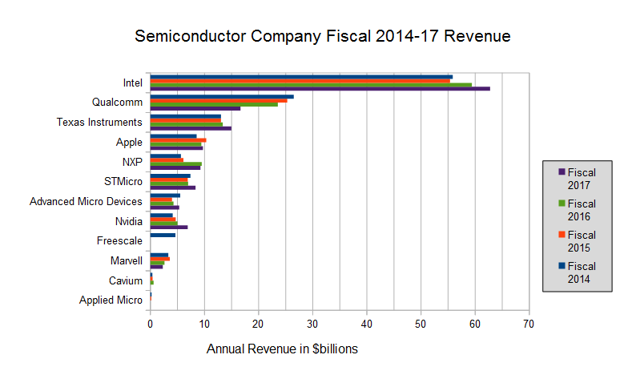

Underlying Apple's ability to grow its iPhone franchise, as well as diversify into wearables, is its expertise in designing mobile processors. Based on a conservative valuation of its systems on chip (SOCs) at $35 a piece for its iOS and watchOS devices, Apple has become one of the larger semiconductor companies in terms of equivalent revenue.

Apple's custom SOCs have been instrumental in the creation of new products such as Apple Watch and Air Pods. There's additional synergy due to the fact that Apple's operating systems developers have access to intimate knowledge about the processors that they wouldn't have if the processors were developed by a separate company. This allows its operating systems to be better optimized and integrated with its hardware.

Apple's custom SOCs have been instrumental in the creation of new products such as Apple Watch and Air Pods. There's additional synergy due to the fact that Apple's operating systems developers have access to intimate knowledge about the processors that they wouldn't have if the processors were developed by a separate company. This allows its operating systems to be better optimized and integrated with its hardware.

Apple is widely expected to introduce some form of augmented reality headset in the near future. I think it likely that these will be in the form of ��smartglasses�� that allow information and graphics to be viewed as an overlay on the real world. Apple's ARKit lays the foundations for this approach, and Tim Cook has expressed his enthusiasm regarding the potential for AR.

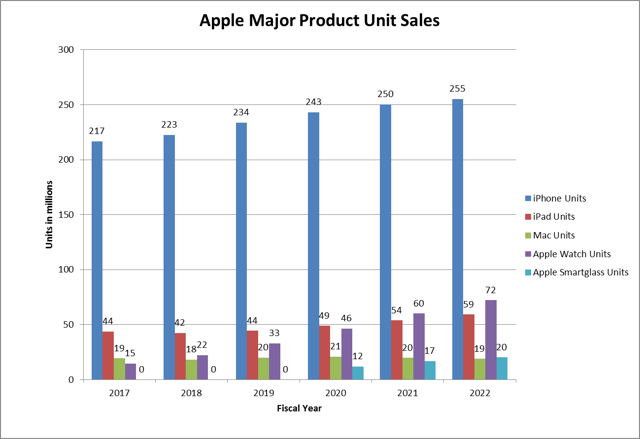

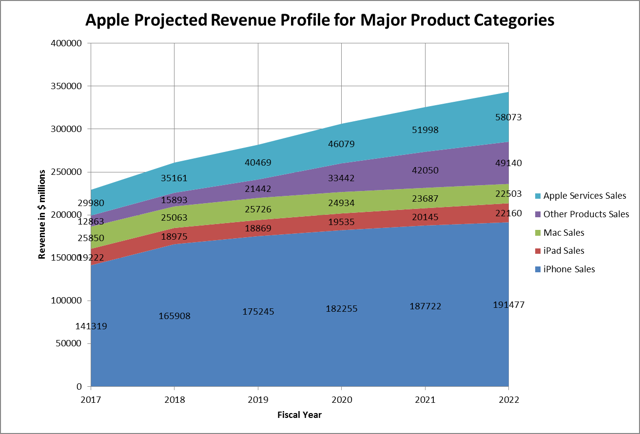

In the chart below, I give my expectations for unit growth in Apple's major products. The numbers for fiscal 2017 are actuals.

DCF fair value

DCF fair value In arriving at a buy rating for a given company in the RT Portfolio, I consider a number of factors, such as the competitive ranking I give above. But certainly, one of the most important, and relevant in terms of assessing valuation, is the Discounted Cash Flow model that is maintained for each Portfolio company. The calculated fair value is used to estimate a percent upside relative to the stock's current price.

I've seen DCF models presented as if they were cast in concrete, but nothing could be further from the truth. DCF model predictions are heavily dependent on the assumed revenue profile of a given company over a long (5-10 year) time frame. Such predictions have inherently large error bars attached to them.

This is why I regard the DCF fair value prediction as only one of many inputs to a final ��grade�� for a given company. In Apple's case, I consider the DCF fair value to be a pretty good estimator of the upside Apple investors can expect.

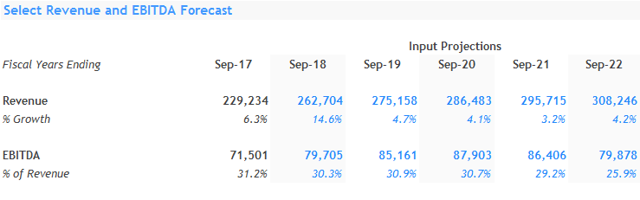

I don't build the models from scratch, but rather download the most recent model from finbox.io. The Apple model covers a five-year period and uses the standard Gordon Growth exit. Shown below are the finbox default Revenue and EBITDA profiles:

The finbox model yields a share fair value of $193.03. In modifying the profiles, I perform a ��ground up�� estimate of revenue contributors, based on the product unit growth shown earlier, as well as other inputs.

The finbox model yields a share fair value of $193.03. In modifying the profiles, I perform a ��ground up�� estimate of revenue contributors, based on the product unit growth shown earlier, as well as other inputs.

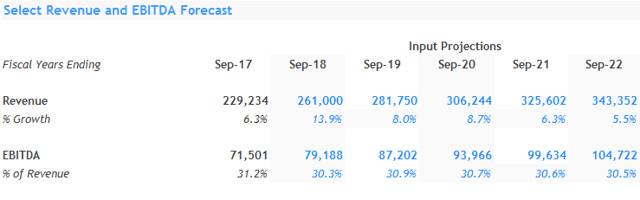

This yields modified revenue and EBITDA profiles shown below:

This yields modified revenue and EBITDA profiles shown below:

The EBITDA profile reflects my expectation that Apple's margins will not decline very much over the five-year period. The resultant share fair value is $239.89. This gives an upside of about 29% compared to the current share price of about $186.

The EBITDA profile reflects my expectation that Apple's margins will not decline very much over the five-year period. The resultant share fair value is $239.89. This gives an upside of about 29% compared to the current share price of about $186.

Do I think that the DCF fair value represents the limit of Apple's growth and upside? I really don't. I regard it as effectively the lower limit, a floor to growth that investors can have high confidence in.

Apple continues to invest substantial R&D in new technologies such as MicroLED displays and autonomous vehicles. It's not clear where this will lead in terms of new products, but I doubt that Apple is engaging in the research without clear product objectives in mind. Autonomous vehicles especially offer the prospect of revenue growth that can ��move the needle�� even for a company the size of Apple. I remain long Apple and rate it a strong buy.

Consider joining Rethink Technology to receive exclusive reports and RT Portfolio updates.

Disclosure: I am/we are long AAPL, TSM, ASML.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

No comments:

Post a Comment